Some stocks deliver quick gains — and that’s always exciting. But the true secret to a successful portfolio always includes those solid players that deliver great performance over the long term. How to find them? When it comes to biotech, I take a good look at the pipeline. That, after all, will determine whether the company has what it takes to generate revenue in the future. I also look at the general financial picture and the company’s strategy. Those elements, too, will influence tomorrow’s performance.

Today, I’ve chosen three biotech companies that already are generating billions of dollars in revenue. But their stories don’t stop here. These players have so much potential that you’ll want to hang onto them for the long haul.

1. Vertex Pharmaceuticals

Vertex Pharmaceuticals (NASDAQ: VRTX) is the leader in cystic fibrosis (CF) treatments. The company’s therapeutics brought in $7.6 billion in revenue last year. Gains were led by its blockbuster Trikafta. And we can expect revenue to keep growing. The only threat to Trikafta’s market share is another Vertex candidate in development. The company recently launched a phase 3 trial of that potential product. So, whether Trikafta keeps its top spot or the new candidate eventually unseats it, Vertex still wins.

eyond CF, Vertex is at an important and exciting turning point. The company aims to submit a request for the regulatory approval of CTX001, its investigational treatment for blood disorders, later this year. The gene-editing candidate is a one-time curative treatment for beta thalassemia and sickle cell disease. Treatment options for these illnesses are limited. So, Vertex’s potential product could be a game-changer.

Vertex shares suffered over the past year or so as investors worried about its ability to succeed beyond CF. But CTX001 and progress on other pipeline candidates are good signs. The stock is trading at only 16 times forward earnings estimates. I consider this a bargain for a solid, long-term stock.

2. Regeneron Pharmaceuticals

Regeneron Pharmaceuticals (NASDAQ: REGN) won big with its monoclonal antibody treatment for COVID-19. It helped the company post an 89% increase in sales last year to more than $16 billion.

Now, I have some good news and some bad news. The bad news is that the antibody treatment isn’t effective against the omicron variant. So, Regeneron doesn’t expect to record more revenue from it in the near term. But here’s the good news. And it comes in two parts. First, Regeneron is working on next-generation antibody candidates to treat emerging variants. And second, even without coronavirus antibody treatment sales, Regeneron is thriving. Excluding that revenue, Regeneron posted a 19% revenue gain last year.

So, with or without a coronavirus antibody treatment to sell, Regeneron has elements that should equal growth. Revenue for blockbuster eye drug Eylea and blockbuster dermatology drug Dupixent is climbing. The company expects regulatory decisions this year on additional indications for Dupixent as well as cancer drug Libtayo.

Regeneron has more than 30 programs in the pipeline. And 11 are in phase 3 — this could result in new products on the horizon if all goes smoothly.

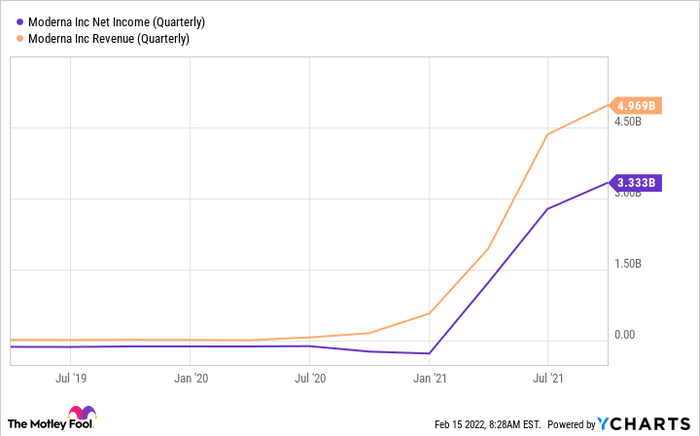

3. Moderna

Moderna (NASDAQ: MRNA) may seem like a short- or medium-term stock if you look at its enormous gains over the past two years. It’s climbed 1,200%. That’s thanks to its development of a coronavirus vaccine, and its ability to generate billions of dollars in revenue and profit.

But there’s more to Moderna than the coronavirus vaccine. And that’s why I think this stock could be a solid long-term play. Moderna has 40 programs in the pipeline right now. Many of them are quite advanced, and some offer blockbuster opportunity. A good example is Moderna’s cytomegalovirus (CMV) vaccine candidate. Moderna launched a pivotal phase 3 trial this fall. Right now, a vaccine for CMV doesn’t exist. And this common virus represents danger for unborn babies and people with weakened immune systems. Moderna could enter the market first — and generate billions of dollars in revenue.

Moderna is focusing on other areas that could generate major revenue too. For instance, it’s working on two HIV vaccine candidates. One recently entered a phase 1 trial. Many companies have failed in the area of HIV vaccines. A win here could be big.

Finally, considering all of this growth potential, Moderna’s shares today are cheap. They trade for only five times forward earnings estimates. So now is a good time to invest in this company that has plenty of potential beyond the coronavirus program over the long term.

Source: MSN Money